Retirement Planning

As you near retirement, you'll have questions and need information. This website will help guide you from your initial thoughts to the first few weeks after your retirement.

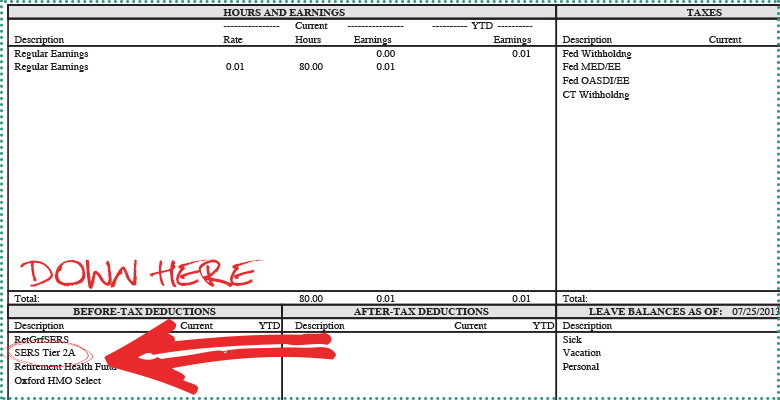

The State of Connecticut has a number of different retirement plans, so — if you're unsure — you'll need to identify your retirement plan. To do so, look at the "Before-Tax Deductions" section of your current paycheck. That will show your retirement plan and the amount you are contributing while working. Once you leave state service, you won't make contributions toward a retirement plan. You can find copies of your recent paystubs in Core-CT.

The chart below shows the minimum requirements to begin collecting a benefit under your retirement plan. Please note that if you are one of the few employees who participates in Teachers’ Retirement (TRB), please visit their website.

| Retirement Plan | Minimum Requirements to Commence Retirement | |

| Alternate Retirement Program (ARP) | ||

| ARP | You have access to your ARP account starting at age 55 if you no longer work for the State of Connecticut in any capacity, including Special Payroll. (Note: If you leave state service with less than 10 years of participation in ARP, there is no minimum age to access your ARP account.) | |

| State Employees Retirement System (SERS) Plans | ||

| Tier I | Non-Hazardous Duty | Age 55 with 10 or more years of actual service |

| Hazardous Duty | Any age following 20 years hazardous duty service | |

| Tier II Tier IIA |

Non-Hazardous Duty | Age 55 with 10 or more years of vesting service |

| Hazardous Duty | Any age following 20 years hazardous duty service | |

| Tier III | Non-Hazardous Duty | Age 58 with 10 or more years of vesting service |

| Hazardous Duty | Any age following 25 years hazardous duty service, or Age 50 with at least 20 years of hazardous duty service |

|

| Tier IV | Non-Hazardous Duty | Age 58 with 10 or more years of vesting service |

| Hazardous Duty | Any age following 25 years hazardous duty service | |

| Hybrid Plan | Refer to underling Tier Plan | |

If you are participating in a Non-Hazardous Duty SERS Plan, it’s important to know that your monthly pension benefit will be reduced if you retire prior to meeting the requirements for a normal retirement. The reduction is ½% for each month early you retire (6% per year). This is a permanent reduction in your monthly pension benefit. Below is a chart that reflects the requirements to retire without a reduction factor.

| SERS Retirement Plan | Normal Retirement Age and Service Requirements | |

| Tier I | Age 55 with 25 years of actual service, or Age 65 with 10 years of service |

|

| Tier II Tier IIA |

Retirement date prior to 7/1/22 or if grandfathered: Age 60 with at least 25 years of vesting service, or Age 62 with at least 10 years of vesting service Retirement date on or after 7/1/22: |

|

| Tier III Tier IV |

Age 63 with at least 25 years of vesting service, or Age 65 with at least 10 years of vesting service |

|

| Hybrid Plan | Refer to underlying Tier plan |

Employees who retire under their retirement plan may also qualify for retiree health benefits if they meet the eligibility requirements. You will need to know your hire date in a position that provides retirement benefits, your years of service, and your retirement plan. You can use the chart below to determine the eligibility requirements that apply to you.

| Hire Date into a Retirement-Eligible State Position | Retiree Health Plan Eligibility Requirement |

| Prior to July 1, 1997 | At least age 55 with 10 or more years of service |

| July 1, 1997 through June 30, 2017 |

Refer to Division Memorandum 2013 |

| On or after July 1, 2017 | If transitioning directly to retirement: - At least age 58 with 15 or more years of service. If voluntarily leaving state service prior to commencing a pension benefit: - 15 or more years of service. Can commence retiree health benefit when age plus years of service total 75 or more (minimum age 58). |

Most people have three sources of income in retirement: retirement plan, Social Security and retirement savings. These benefits will vary based on the retirement date you select. Online estimators help you project what you will receive based on the retirement dates you enter.

Income Based on the Retirement Plan in Which You Participate

ARP

You have many withdrawal options available, including the option to purchase an annuity that provides you with a monthly benefit for life. More information is available at www.ctdcp.com.

SERS Tier Plans

You collect a lifetime monthly pension benefit based on a formula that takes into consideration your age, years of service, and average earnings. At retirement, you will select one of the following survivor payment options: Straight Life Annuity (no survivor benefits payable); 50% Spouse; 50% or 100% Survivor; 10- or 20-Year Period Certain. The amount of your monthly pension benefit is adjusted under each of these payment options. The State provides an online estimating tool and more at the following website: https://www.osc.ct.gov/rbsd/stateretire.htm.

Hybrid Plans

You have an option at retirement. You can collect a monthly pension benefit for your lifetime (same as the SERS Tier Plans) or you can cash out your pension.

Social Security Income

You can start receiving your Social Security retirement benefits as early as age 62. However, you are entitled to full benefits when you reach your full retirement age. The following is a link to a chart that reflects your full retirement age based on your date of birth: https://www.ssa.gov/benefits/retirement/planner/agereduction.html. If you delay taking your benefits from your full retirement age up to age 70, your benefit amount will increase.

Social Security Administration provides an online tool that you can use to estimate your monthly benefits using different dates at the following website: www.ssa.gov.

Retirement Savings

The State offers employees tax-favored savings programs to help save for retirement: 403(b), Roth 403(b), 457 and Roth 457. For information about accessing these funds in retirement visit www.ctdcp.com.

Employees who retire and qualify for retiree health insurance can use the charts below to determine the current costs in retirement. It’s important to note that employees who retire early contribute more until they reach their normal retirement age. Participants under age 65 have the same medical options available to employees. Participants age 65 and older are covered under a Medicare Advantage Program through Aetna.

Early Retirees

Minimum 10 years of service at age 55, except age 58 for SERS Tier 3 and 4

Employees who retire prior to their normal retirement pay a higher share of the premium each month until they reach their normal retirement age. The percentage of the premium they pay is based on their years of service and how early they are retiring, as is shown in the chart below.

| Percentage of Total Premium Paid by Early Retirees | |||||

| Years Early | |||||

| Years of Service | 5 or more |

4 |

3 |

2 | 1 |

| 15 or less | 40.0 | 32.0 | 24.0 | 16.0 | 8.0 |

| 16 |

37.0 | 29.6 | 22.2 | 14.8 | 7.4 |

| 17 |

34.0 | 27.2 | 20.4 | 13.6 | 6.8 |

| 18 |

31.0 | 24.8 | 18.6 | 12.4 | 6.2 |

| 19 |

28.0 | 22.4 | 16.8 | 11.2 | 5.6 |

| 20 |

25.0 | 20.0 | 15.0 | 10.0 | 5.0 |

| 21 |

22.0 | 17.6 | 13.2 | 8.8 | 4.4 |

| 22 |

19.0 | 15.2 | 11.4 | 7.6 | 3.8 |

| 23 |

16.0 | 12.8 | 9.6 | 6.4 | 3.2 |

| 24 |

13.0 | 10.4 | 7.8 | 5.2 | 2.6 |

| 25 or more |

10.0 | 8.0 | 6.0 | 4.0 | 2.0 |

The premium percentages are prorated by months. The percentage at retirement applies to all years early (no adjustment each year).

After you identify your percentage from the chart above, you multiply it by the Total Premium. Below is the chart that reflects the total monthly premiums for the 2024-2025 plan year. Retirees can change their option each year during the annual open enrollment. Please note that these are the premiums for persons who are under age 65. Select the column based on the number of persons you are covering who are under age 65. Note: Persons age 65 and older will have a different plan, which is described in the section Retirees/Spouses Age 65 or Older.

| 2024-25 Total Monthly Premiums for Persons Under the Age 65 |

|||||

| Anthem Blue Cross Blue Shield |

1 Person | 2 People | 3+ People | ||

| Expanded Access (POS) | $1,320.97 | $2,906.14 | $3,566.62 | ||

| Standard Access (POE) | $1,296.06 | $2,851.33 | $3,499.36 | ||

| Primary Care Access (POE-G) | $1,284.43 | $2,825.75 | $3,467.96 | ||

| Anthem State Preferred | $1,405.96 | $3,093.11 | $3,796.09 | ||

| Anthem Out of Area |

$1,405.96 | $3,093.11 | $3,796.09 | ||

| Quality First Select Access |

$1,224.25 | $2,693.35 | $3,305.47 | ||

It’s important to note that if your result is more than 25% of your actual monthly pension benefit, you will pay 25% of your monthly pension benefit (Cap), unless you work less than full time. The actual pension benefit will be prorated for employees who are less than full time.

Employee retires 2 years early with 20 years of service and is enrolled in the Anthem POE family coverage and has an actual pension benefit of $1,400/month.

Maximum Payable: $1,400 (actual monthly pension) x 25% = $350

Factor from Table: 10% (payable for 2 years prior to normal retirement age)

Total Premium from Chart for Anthem POE: $3,362.60

Monthly Premium: $3,362.60 x 10% = $336.26 (below the maximum)

Normal Retirees

Minimum age* If less than 25 years of service: 62 (Tier 2, 2A), 65 (Tier 1, 3 and 4)

Minimum age* with 25 years or more of service: 55 (Tier 1), 60 (Tier 2, 2A), 63 (Tier 3, 4)

Retirees have an open enrollment each year in which they can make changes to their elections. The State provides employees with the Retiree Health Care Options Planner each year, which includes the monthly costs. Below are the premiums paid by employees for the medical options at normal retirement age.

*If Grandfathered Normal Retirement Date

| 2024-2025 Monthly Retiree Premiums for Participants Under Age 65 at Normal Retirement |

||||||

| Coverage Level | Quality First Select Access (State BlueCare Prime Tiered POS) |

Primary Care Access (State BlueCare Point of Enrollment Plus (POE-G Plus)) |

Standard Access (State BlueCare Point of Enrollment (POE)) |

Expanded Access (State BlueCare Point of Service (POS)) |

Anthem State Preferred POS* |

Anthem Out- of-Area |

| 1 person | $61.21 | $64.22 | $64.80 | $66.05 | $70.30 | $70.30 |

| 2 persons | $134.67 | $141.29 | $142.57 | $145.31 | $154.66 | $154.66 |

| 3+ persons | $165.27 | $173.40 | $174.97 | $178.33 | $189.80 | $189.80 |

Retirees/Spouses Age 65 or Older

Retirees and their spouses who are age 65 or older have one plan option in retirement, the Aetna Medicare Advantage Program. To qualify for this plan, the person must be enrolled in both Medicare Part A and Medicare Part B on the first of the month following their retirement date. Please note retirees and spouses age 65 or older must enroll for Medicare Part A and B with Social Security and must provide proof of enrollment to the State. The State will then handle the enrollment in the Aetna Medicare Advantage Program and Medicare Part D.

The Aetna Medicare Advantage Program is a full replacement to Medicare and was designed to closely resemble the out-of-pocket costs of the active employee coverage. There is no premium required for this plan.

Below is a chart that shows what Social Security will charge participants each month in 2024 for enrollment in Medicare, which is based on a person's 2022 income tax return. Please note that the State will reimburse the retiree and spouse 100% of the Base Rate for Medicare Part B and 50% of the IRMAA rates for Parts B and D.

| Yearly Income in 2022 | Participants pay each month (in 2024) |

||||||

| File Individual Tax Return |

File Joint Tax Return |

File Married & Separate Tax Return |

Part A | Base Rate for Part B |

Income Related Adjustment Amount (IRMAA) for Part B |

Part D (Prescription Drugs, DO NOT ENROLL; State will handle the enrollment) | Total per Person/Month |

| 103,000 or less | $206,000 or less | $103,000 or less | $0 | $174.70 | $0 | $0 | $174.70 |

| above $103,000 up to $129,000 | above $206,000 up to $258,000 | Not applicable | $0 | $174.70 | $69.90 | $12.90 | $257.50 |

| above $129,000 up to $161,000 | above $258,000 up to $322,000 | Not applicable | $0 | $174.70 | $174.70 | $33.30 | $382.70 |

| above $161,000 up to $193,000 | above $322,000 up to $386,000 | Not applicable | $0 | $174.70 | $279.50 | $53.80 | $508.00 |

| above $193,000 up to $500,000 | above $386,000 up to $750,000 | above $103,000 up to $397,000 | $0 | $174.70 | $384.30 | $74.20 | $633.20 |

| $500,000 or above | $750,000 and above | $397,000 and above | $0 | $174.70 | $419.30 | $81.00 | $675.00 |

Information about the Aetna MedicareSM Plan (PPO) can be found here.

Dental

Retirees have the same dental options as active employees, but they pay a higher share of the cost. There is an annual open enrollment period in which retirees can change their dental elections. The premiums are published in the annual Retiree Health Care Options Planner.

| 2024-2025 Monthly Retiree Dental Premiums | ||||

| Coverage Level | Dental Care DHMO Plan | Total Care DHMO Plan | Enhanced Plan | Basic Plan |

| 1 person | $23.38 | $29.16 | $35.09 | $43.71 |

| 2 persons | $51.45 | $64.15 | $70.18 | $87.42 |

| 3+ persons | $63.14 | $78.74 | $70.18 | $87.42 |

Retiree Health Care Options Planner

From the Office of the State Comptroller, review the 2024 - 2025 Retiree Health Care Options Planner.

If you or your spouse will be age 65 or older when you retire, read more about how the insurance benefits work.

Human Resources developed a Checklist and Guidelines to give employees a better understanding of what happens when leading up to retirement and the weeks following retirement.

Retirement Paperwork

- You can submit the Retirement Initiation Packet at any time prior to your retirement, but ideally at least three months prior. Your signed retirement forms cannot be dated more than 90 days prior to your retirement date.”

- HR will prepare forms for your signature, and will contact you once they are available. Sign, date, and return retirement forms to HR with Required Proof Documents. Forms require original signatures on single-sided pages. The earliest employees can submit signed retirement paperwork is 3 months prior to retirement.

- For employees or spouses aged 65 or older, HR will send you forms to file for Medicare Part B. You file the paperwork directly with your local Social Security office requesting a coverage effective date of the first of the month following retirement.

- Contact Prudential for information on how to defer the tax liability of any final payout. Your final paycheck will automatically include the payout of accruals. Human Resources recommends employees pursue this step a month before retirement.

- If not yet done, provide written notice to your department of your retirement.

Required Proof Documents Needed at the Time of Retirement

The State requires that employees provide copies of the following proof documents with their retirement application.

Birth Certificates

For employee, your spouse (or Contingent Annuitant) and each child to be enrolled in retiree health benefits

- The name on the birth certificate must match the name on the retirement forms, or be the maiden name as reflected on the marriage certificate (for married participants).

- If the name is different, court documents can be provided as proof of a name change or the person can complete a Name Affidavit.

- If the birth certificate is not in English, a certified translation must also be provided.

- The State will not accept birth certificates from Puerto Rico issued prior to July 1, 2010.

- Persons born outside of the US who do not have a birth certificate must complete a Birth Affidavit.

Marriage Certificate

For married employees

- If the marriage certificate is not in English, a certified translation must also be provided.

- Marriage notices from the church are generally not acceptable as proof of marriage. The exception is when they are certified by the town/city in which the marriage occurred.

- Employees married outside of the US who do not have a marriage certificate must complete a Marriage Affidavit.

Medicare Card

For retirees and spouses age 65 and older who will be enrolled in retiree health benefits.

The Medicare Card does not need to be provided in advance of retirement. Retiree health benefits are effective the month following retirement. The Medicare card is proof of enrollment and is required for reimbursement of Medicare Part B premiums.

Letter from Social Security with Medicare Part B Premiums

For retirees and spouses age 65 and older who will be enrolled in retiree health benefits.

This letter does not need to be provided in advance of retirement. If you are a higher wage earner who will be subject to an Income Related Monthly Adjustment Amount (IRMAA), you will want to provide a copy of the letter that reflects the IRMAA amount.

Final Paychecks

Employees generally receive two paychecks following retirement. The first paycheck will be a standard biweekly check. The second will be your final paycheck and will automatically include the payout of accruals.

Receipt of New Medical ID Cards

Retiree health benefits begin on the first of the month following retirement. During the first month of retirement, continue to use your active employee cards. If you or your spouse received a new Medicare Card showing enrollment in Part A and Part B, send a copy to your Human Resources retirement specialist as proof of enrollment, and a copy of the letter from Social Security reflecting Part B costs to be reimbursed.

SERS Pension Benefit

SERS participants will receive a letter from the Retirement Services Division by the end of the first month of retirement identifying the amount of their monthly pension benefit. Pension checks are dated on the last business day of the retirement month. Retirees have online access to pension checks and will be provided access information by the Retirement Services Division.

Payroll Deductions

Contact Information

Human Resources will not have access to your retiree health benefits or your pension check. Contact the appropriate department at the Office of the State Comptroller with any questions you have. Contact information.

Reemployment Options

Reemployment in a Temporary Position at UConn Health

Under the provisions of the Policy on Re-Employed Retirees, the University may offer retirees an opportunity to return to or remain at UConn Health on a part-time basis. Refer to the policy for further information and details. Reemployment is the prerogative of UConn Health and not an employee entitlement.

Reemployment in a Permanent Position

If you are reemployed by the State in a permanent position after you have retired, your SERS pension payments and retiree health and life insurance benefits will cease. You must notify the Retirement & Benefits Services Division of your reemployment. You will resume membership in your SERS plan and receive credit for service during your reemployment. When you next retire, your SERS retirement benefit will be recalculated and will not be less than the amount you were receiving prior to reemployment.